Life Insurance Buying Process – Guide to Purchasing Life Insurance

Objective

In this module

-

You will better understand what to look for when purchasing life insurance, along with the general purpose of life insurance and the many different needs it can fulfill.

-

You will be able to begin the process of clarifying and quantifying your needs for purposes of calculating how much life insurance you actually need.

-

You will learn about the two primary types of life insurance – Term and Permanent – and how they differ in providing coverage.

-

You will learn about the life insurance purchasing process and how to obtain the right coverage for your needs.

Overview

The primary reason life insurance is purchased by consumers is to provide the financial security their family needs when one of the primary breadwinners dies prematurely. To that end, it forms the foundation of a family’s financial plan. But, the unique properties of life insurance give it a distinct versatility that makes it a suitable solution in many different financial situations.

Generally, individuals and businesses will buy life insurance policies to meet a number of different needs including:

- Family protection and income replacement

- Tax-favored accumulation for long term savings goals

- Estate transfer costs and taxes

- Leaving a legacy

- Business buy-sell arrangements

- Keyperson protection for a business

- Business continuation

- Funding deferred compensation for business owners and key employees

How Much Life Insurance do you Need?

For most people, the difficult decision is not “if” they need life insurance, but “how much” life coverage they need. It’s a much bigger decision, and one that can lead to consternation over the purchase decision if it is not made with the proper consideration. Buying too much life insurance has always been a concern for people who don’t like paying for what they don’t need, and buying too little insurance can lead to a lot of sleepless nights and disaster for the surviving family.

At its simplest, knowing how much life coverage you need should be based on precisely what the “needs” are. Needs can and should be quantified so that the amount of life coverage can be determined with relative accuracy. Only then can you be assured that you own the right amount of coverage.

Clarifying Your Need

For a family, the list of needs may not be extensive, but they should be very clearly defined.

- Debts – including mortgages, credit cards, personal loans

- College expenses – determine cost of college education and how much to be funded

- Final expenses – including final medical costs, funeral expenses, legal fees

- Income replacement – determine surviving spouses earning capacity and the amount of income needed during and after dependency years.

Quantifying Your Need

Once the needs are clearly defined, they need to be priced, meaning their current costs need to be determined. This is easy to do for lump sum requirements such as debt payoff. Even for future costs such as college expenses, it’s easy if you use today’s costs and then apply an inflation factor. But, the most practical way to measure any cost is to assume that death occurs immediately. As long as you apply a reasonable capital growth assumption for the proceeds that are invested to cover future costs, it should be sufficient when planning in today’s terms.

Calculating income needs is a little more complicated. The income needed while the children are dependent will obviously include child-rearing expenses including clothing, food, recreation, education, medical, child-care and miscellaneous outlays. The non-dependency years of your spouse will require less income, but should be sufficient to allow for a continuity of lifestyle. Again, the time horizon for the need is important, and if your spouse is not a primary bread-winner, it is never safe to assume that your income will be replaced by his or her own earnings which may not materialize in the manner or time frame you might hope for.

For each stream of income – one for the dependency years, and one for the non-dependency years, the calculation is made by totaling the income required for each period and then discounting it to a present value using a conservative interest factor. This will generate the amount of money needed today to produce the required income based on it earning an assumed rate of return. The more conservative you are with your assumptions, the greater the cushion that can be created for added security.

Hypothetical Capital Needs Analysis -Husband (38) and wife (35) with two kids (2 and 4)

Lump Sum Cash Need:

| Debt | $550,000 |

| College Funding (present value invested at 5%*) | $ 50,000 |

| Final Expenses | $ 30,000 |

| Total Lump Sum Cash Need | $630,000 |

Income Replacement Need:

| Current Family Income | $250,000 |

| Income lost at death of primary breadwinner | $200,000 |

| Income replacement during child dependency years (15 years) assuming debt and college expenses paid off | $2 million |

| Income replacement during non-dependency years until retirement (20 years) | $ 3 million |

| Present value of the two income streams invested at 5%* | $1.2 million |

| Total Capital Need (Lump sum cash needs + Income replacement) | $1.38 million |

*5% is a hypothetical return and is not guaranteed

Determining Your Coverage Amount

Click for

INSTANT LIFE INSURANCE QUOTES

With your needs clarified, quantified, and their costs determined, you can then apply your existing resources as offsets to determine what is left uncovered. For instance, if you have existing life insurance, savings, or investments, these assets are available to offset the need for additional life coverage. If you have additional income sources, such as your spouse’s current income, income from a trust or rental property, it can be used to offset the income need.

Capital Available

| Cash/Savings | $ 50,000 |

| 401(k) Plan | $225,000 |

| Group life insurance | $350,000 |

| Total Capital Available at death | $625,000 |

Total Life Insurance Need

| Total Capital Need less Total Available Capital | $1.2 million |

Following this process you will be able to arrive at a coverage amount that provides you with the assurances that you have bought the right amount and that your family will be secure. The process described here can be carried out on a few sheets of graph paper, or with the use of any number of financial calculation tools that are available for free on the internet.

Feel free to visit our website, insuringincome.com, where you can find life insurance calculators and instant life insurance quotes.

Types of Life Insurance Policies

All of the various forms of life insurance – whole life, term life, variable life, universal life and the dozens of variations of each – can be distilled down to just two types: Term and Permanent. As their names would imply, term is life insurance that covers a certain term or number of years, and permanent is life insurance designed to remain in place as long as premiums are paid.

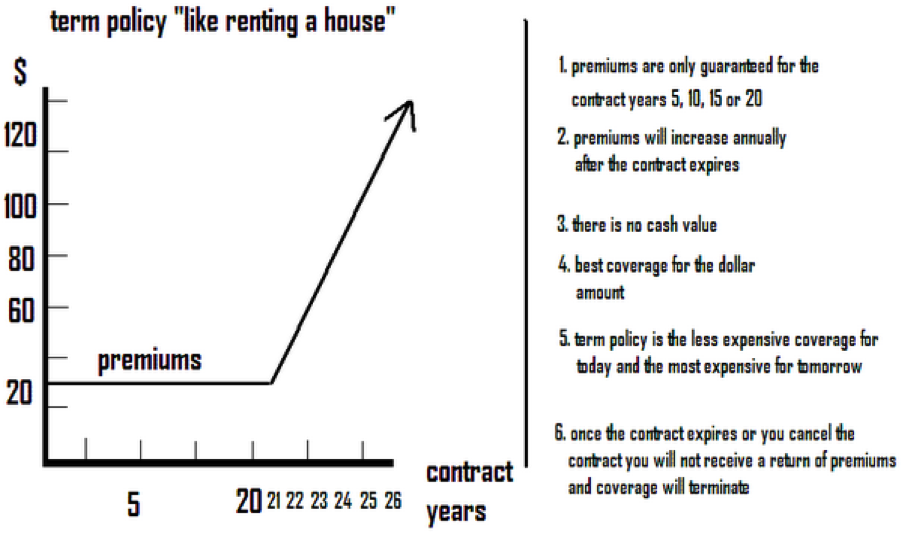

Term Life

Because of its lower premium, term life insurance is a popular choice for people who believe it can provide the greatest amount of coverage at the lowest overall cost. While that may be true if you knew when you were going to die, it doesn’t necessarily hold true if you die closer to the age that the insurance company expects you to die.

As the graphic illustrates, a level term policy can provide a level death benefit for a certain period of time – i.e., to age 65, 10 years, 15 years, 20 years, 25 years, or for 30 years – after which your premium stops and your death benefit stops. If, at the end of that period of time, you still have a need for life insurance protection, you would have to renew the coverage at a much higher rate, often prohibitively high; that is if you are still insurable.

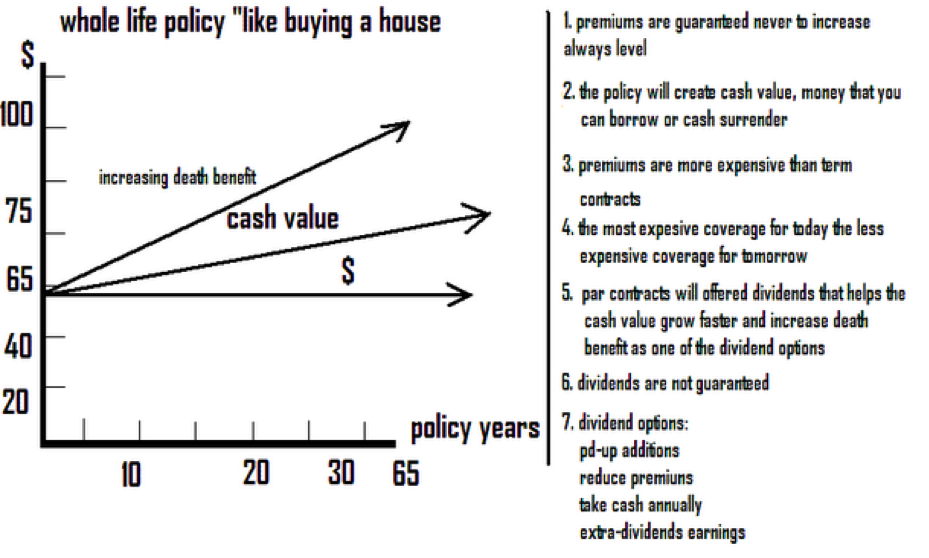

Permanent Life Insurance

Permanent life insurance, also referred to as whole life insurance, is designed to provide protection for your whole life. As long as the premium payments are made, it will continue to provide protection and it can never be cancelled. As the graphic illustrates, a typical whole life product starts out providing a level death benefit that, when a level premium is paid over time, will increase. This is due to the cash value element of whole life which guarantees a minimum rate of growth on the portion of the premium that isn’t applied to the cost of insurance. Because there has to be a certain space between the cash value and the death benefit, the cash value growth automatically pushes the death benefit higher.

Quick Comparison of Term versus Whole Life

|

Term Life Insurance |

|

Whole Life Insurance |

|

|

|

||

Purchasing Life Insurance

Click for

INSTANT LIFE INSURANCE QUOTES

Once you initiate the buying process with a life insurance provider, the process takes on a life of its own. It begins with the completion of an application, so it is helpful to have all of your financial and medical information at hand. The application will ask you about your current financial situation and it will inquire about your medical history. You will also need to agree to a release of your medical records.

The application is also where you will begin to piece together the different components of your policy, including the death benefit amount, your beneficiaries, policy riders, dividend options or investment selection, and you mode of payment.

The application is submitted for review by underwriters. If a medical exam is required (this will depend on your age, the amount of life insurance, and your medical history), it is scheduled. The exam is usually done by a paramedical professional who comes to your home or office. Your exam results are submitted to the underwriters for review. After all of the medical records and the exam have been reviewed, the policy is issued. From the time of application to the time of policy issue it can take from 60 to 90 days depending on how quickly your medical records are transferred.

After you receive the policy and pay the first months’ premium, you have free look period of 30 to 60 days to carefully review the contract and the policy provisions.

Helpful Tips

- Find a reliable life insurance specialist with whom to work. They will take on the responsibility of getting you from application to policy issue with the least amount of friction. They can also be invaluable during times when you need any sort of service on your policy. It can be critical to work with a company that can go to multiple life insurance companies as health history can cause one carrier to approve with a less than favorable health rating.

- Buy from the best. Make sure you submit your application with a company that is highly rated for their financial strength and claims paying ability. Check their ratings from A.M. Best (A rated or better) and Standard & Poor’s’ (AA rated or better).

- If an agent or broker recommends more life insurance than you calculated for yourself, be sure to get a complete audit of their calculation and have them validate their reasoning.

- If a product other than what you were considering is recommended, ask for a detailed cost-benefit comparison of the two types of policy and a written explanation as to why it was recommended.

Buying a life insurance policy can be an intimidating experience, which is probably the reason why so many people procrastinate. Armed with this fundamental knowledge about your own needs, the different types of policies and how the process works, you should be able to enter the process in control and with greater assurance that your life insurance needs will be met.

Key Takeaways

-

Because it provides the capital needed before the breadwinners can accumulate sufficient capital of their own, life insurance is considered to be the essential foundation of a financial plan.

-

Life insurance coverage should be based on actual needs and not general rules of thumb or simple formulas.

-

Term life insurance provides maximum coverage at the lowest cost

-

Whole life or permanent insurance requires a higher premium because it’s designed to pay off, either at death or during your lifetime (cash value).

-

It’s best to work with a financial professional who specializes in life insurance and who can provide objective advice in formulating a life insurance plan best suited for your needs.

Click for

INSTANT LIFE INSURANCE QUOTES